Why Profitability in Asia’s Agri-Input Sector Remains Elusive

Why Profitability in Asia’s Agri-Input Sector Remains Elusive

(And What to Do About It)

Why Asia's Growth Potential Isn’t Translating to Profit Margins

Asia represents the world’s most significant agri-input opportunity, as a home to half the global population, rising food security needs, and increasingly sophisticated farming practices.

Yet despite strong growth potential, many input providers struggle to convert this into sustainable margin gains.

What’s behind the disconnect?

- Fragmented, high-cost markets with uneven service expectations

- Persistent smallholder access and affordability constraints

- Rising competitive pressure from generics; both ‘me too’ and ‘me better’ products

- Localized agronomy needs limiting economies of scale

Profitability in Asia’s agri-input markets will not be achieved just by growing the topline, it’s about managing the product portfolio actively, transforming how companies go to market and operate.

What Leading Players Are Doing Differently

Across the region, companies are shifting from uniform commercial strategies to differentiated market approaches, treating each country (and regions within giants like China or India) as its own profit system.

Common strategic responses

Growth markets - scale-up with leaner, fit-for-purpose cost structures and GTM transformation. Example: Direct sales in India’s Haryana/Punjab; distributor + eCommerce in the fragmented Eastern corridor.

Mature markets - structural cost resets and GTM reinvention. Example: moving from direct sales to 100% industrial partner-led in Northeast Asia delivered +20% EBIT in Year 1.

Mixed-margin markets - product mix optimization, pricing discipline, and GTM focus. Example: brands below a profit threshold phased out, licensed, or handed to partners with broader reach.

This archetype-driven approach moves companies beyond revenue focus and into EBIT-focused execution.

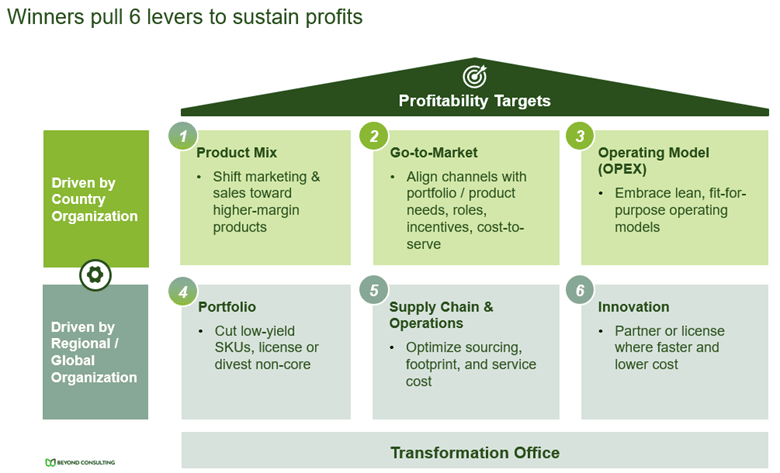

Six Levers That Drive Results

Improving profitability in Asia is less about inventing new levers, and more about sequencing and localizing well-known ones. Six levers matter most – as shown in the below chart - with some best pulled at the country level (Mix, GTM, OPEX), and others requiring regional or global orchestration (portfolio, supply chain, innovation). The balance between the two is what drives sustainable EBIT impact.

Illustrative case studies

China: Shifting from direct-serve to a hybrid RTM (e.g. Key Account / National Distributors / Regional Dealers / eCommerce) while focusing direct sales efforts on high margin products in highest ROI counties cut cost-to-serve and improved EBIT resilience.

Northeast Asia: Moving from direct sales to an industrial partner-led model (regional GTM redesign) cut cost-to-serve and lifted EBIT +40% in Year 1.

These are not new ideas - what matters is how they are sequenced, localized, and governed across diverse markets. A Transformation Office acts as a hub that helps tracks milestones, drives accountability, and ensures country and regional levers deliver EBIT impact in sequence.

Execution Insights from the Field

The most successful programs we’ve seen in Asia treat profitability as one P&L with two perspectives: regional ambition + country-led delivery.

They use market-specific playbooks rather than one-size-fits-all. Country teams require empowerment and accountability. Transformation is not a top-down rollout.

And they drive disciplined execution from day one, with roadmaps, milestone tracking, and business impact reviewed in short cycle (weekly to bi-weekly); no top-down rollouts, no slideware.

Final Thought

In Asia’s agri-input space, profitable growth doesn’t come from working harder, it comes from working smarter: choosing the right combination of levers, sequencing them thoughtfully, and ensuring execution starts on day one.

Would you like to discuss where the EBIT is in your portfolio and markets?